Credits and Debits... I know what most of you are thinking; that sounds like a fascinating topic. NOT! Therefore, I will make this succinct and to the point. What I really want to give you is a place (this blog posting) you can refer to when you need to know what happens when you debit certain accounts and what happens when you credit certain accounts. Most of the time, you need not be concerned with this as QuickBooks handles most debits and credits in the background. At least one exception to this would be when you need to record a General Journal Entry (JE). The primary purpose of a JE is when you need to record both the debit and credit side of a transaction. A very common example of this would be if you have purchased a vehicle for your business and this vehicle is being financed by the bank. How do you get the principal balance of the loan on the books as well as the value of the Fixed Asset? If you guessed Journal Entry, you are correct. A bit more on the specifics in just a moment. Bur first, let me layout for you what happens to various G/L (General Ledger) accounts (think Chart of Accounts) when you debit or credit them using a JE:

| Account Type | Debit | Credit |

| Bank | Increases Balance | Decreases Balance |

| Accounts Receivable | Increases Balance | Decreases Balance |

| Other Current Asset | Increases Balance | Decreases Balance |

| Fixed Asset | Increases Balance | Decreases Balance |

| Other Asset | Increases Balance | Decreases Balance |

| Accounts Payable | Decreases Balance | Increases Balance |

| Credit Card | Decreases Balance | Increases Balance |

| Other Liability | Decreases Balance | Increases Balance |

| Long Term Liability | Decreases Balance | Increases Balance |

| Equity | Decreases Balance | Increases Balance |

| Income | Decreases Balance | Increases Balance |

| Cost of Goods Sold | Increases Balance | Decreases Balance |

| Expense | Increases Balance | Decreases Balance |

Now, the above may seem a bit weird to you unless you studied accounting in the past. I mean, after all, when the bank gives you a Debit Card and you use this card and certainly does not increase your bank balance; it decreases your balance (at least mine does). Yet, in the accounting world, when you debit a bank-type account it increases the balance. Really? Really!

So refer back to this blog when you want to know what impact a debit or credit will have on various types of accounts. The other option is to simply take a guess. I'm serious. You have a 50/50 chance of being right. If you get it wrong, go back to the JE and switch the incorrect debit and credit.

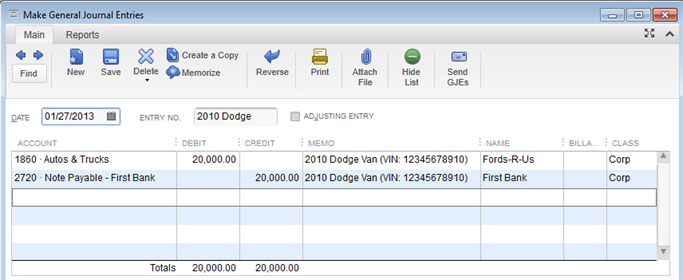

Now, let's go back to the need for that JE we were discussing earlier. Let's say you purchased a $25K van for your business. You wrote a check from your business bank account for $5K. In the check you would post this to a Fixed Asset account called Autos & Trucks. Once done, you have a Vehicle recorded as a Fixed Asset. But the vehicle total purchase price was $25K and that's what your books need to reflect as a Fixed Asset. The remaining $20K balance is the amount financed at your bank. To handle this part, simply record a JE (go to Company, Make General Journal Entries) as follows:

The above entry will result in a loan showing up on your Balance Sheet for $20K (the account type for the loan is a Long Term Liability) and as result of the JE above, coupled with the $5K check you recorded earlier, you will show a Fixed Asset for $25K. Make sense?

If the above helps you, please leave a comment telling us so. If you need further explanation, or have additional questions leave a comment and we will respond. Of course, you can always call us at QuickTrainer, Inc. by dialing (910) 338-0488. You can email us at info@quicktrainer.biz. Remember, we are here to help you with all of your QuickBooks needs.

#ilm